When people are in the working part of their life, they receive regular paychecks to pay their monthly expenses. But after retiring, these regular paychecks are gone. So, when people are nearing retirement, a common question is:

"How can I best position my assets to provide me with a monthly income to pay my expenses during retirement?"

It is a simple question, but no simple answer or plan works for everyone.

When withdrawing money to pay monthly expenses during retirement, the sequence of which assets are used first and how much is taken out of each asset is very important. When creating a retirement income plan, the difference between a bad plan and an optimized plan can result in a difference of hundreds of thousands of dollars by the end of a person’s life. In this blog, we will discuss assets that can be used to create monthly income in retirement, how different retirement goals can affect your plan for retirement income, and issues and strategies to consider when creating your plan for providing income during retirement.

In this blog, you'll learn:

- Sources of Income in Retirement

- Social Security Income

- Income From Retirement Accounts

- Annuities Can Provide Guaranteed Income

- Other Sources of Monthly Income

- Paying Taxes During Retirement

- What if Tax Rates Go Up in the Future?

- What About IRMAA?

- Should I Do a Roth Conversion?

- How Do Market Corrections and Recessions Affect My Plan?

- How Do I Find the Best Retirement Income Plan for Me

Sign up for our email newsletter for views of the economy, stock market, and top news stories from our Wealth Managers at Financial Journey Partners.

Sources of Income in Retirement

People may use many different types of assets and income sources to get income during retirement. Some of the most common include:

- Social Security

- 401(k)

- Traditional IRA

- Roth IRA

- Pension

- Annuity

- Inheritance

- Non-retirement accounts (such as a Trust account)

- And others …

The taxation of these sources is different. If you have several on this list, the challenge is determining when to draw income from each source. The sequence of drawing money for income from your assets can significantly impact how much money you have left later in life. It can also greatly impact the level of taxes you will pay over a lifetime. Let’s talk briefly about how each of these income sources can be used as part of your retirement income plan.

Social Security Income

When we think of income for your retirement, the first thing that may come to mind is Social Security. According to the Social Security Department, “You can start your retirement benefit at any point from age 62 up until age 70. Your benefit will be higher the longer you delay your start date. This adjustment is usually permanent. It sets the base for the benefits you will get for the rest of your life.” Once you begin receiving your benefits, the amount will go up based on inflation each year. So, everyone should claim and receive income from Social Security by age 70. The best time to start drawing your Social Security benefit between ages 62 to 70 depends on your situation.

Most people want to start Social Security at the age where they maximize the amount they receive over their lifetime. Part of the equation is estimating how long you might live. Some have known health issues, so it would make more sense to start Social Security at a younger age, while other people may be healthy and decide to work longer, and they can delay taking Social Security until they retire.

The best time for people to start drawing Social Security depends on their situation. We recommend completing a comprehensive financial plan that includes an analysis to determine the best time for you to begin claiming Social Security.

Income From Retirement Accounts

You may have retirement savings in a 401(k) account at your employer. These are great vehicles for saving money for retirement while you are working. You can save money into a 401(k) pretax, let the money grow inside the account, and then pay taxes on the money as ordinary income when it is withdrawn. 401(k) accounts are not designed to provide automated monthly income once you retire. Most people roll over their 401(k) to an IRA and then use the IRA to send money to your bank account each month to pay your expenses. If you were saving money in your company’s 401(k) plan to your personal post-tax account, then this money can be rolled over to your own Roth IRA.

Companies provide pensions with monthly payments for the rest of an employee's life after they retire. Today, very few public companies provide pensions for their employees. Most companies replaced pensions with 401(k)s. Federal, state, county, and city government agencies still provide pensions for many of their workers. Pensions are still common for teachers and police officers.

Annuities Can Provide Guaranteed Income

There are many types of annuities, and there are too many to describe here. The important point about an annuity is that it can take an amount of your money and create a monthly income that an insurance company will guarantee to pay you for the rest of your life, no matter how long you live. If you are married, an annuity can pay you a guaranteed income for as long as you or your spouse live. With pensions becoming less common, annuities can be a replacement to create a guaranteed monthly income for the rest of your life.

Other Sources of Monthly Income

Some people are fortunate to get a sizable inheritance from parents or other family members. This money can be invested at a financial institution or bank and set up to send a monthly amount to your checking account to pay your expenses. You may have an investment account that is not an IRA that could be titled as a Trust account, a joint account with your spouse, or an individual account that is just in your name. This type of account can also be set up to send you a monthly amount to your checking account.

There are other methods of setting up monthly income, such as purchasing a rental property and using the rent you receive to pay your monthly expenses. When in the right location, that rental property could also increase in value. There are many advantages to investing in real estate. There also tends to be more complications with rentals so be sure to hire trustworthy professionals to help you with these types of investments.

With all these different ways to receive income during retirement, you may have questions such as:

- Which sources of income are best for my situation?

- If I have different sources of income, how much do I take from each?

- Which income sources should I start withdrawing from first?

To answer these questions, the next step is to look at your situation and understand your goals.

Paying Taxes During Retirement

The goals people have regarding paying taxes on their retirement money can vary significantly based on their situation. Some clients have told us they want to pay the minimum in taxes when money is withdrawn from their retirement money and delay paying taxes as long as possible. These people may be in high tax brackets or prefer not to pay taxes. The problem with delaying taxes as much as possible is that if the person has a large IRA, their required minimum distributions in their later years can push them into higher tax brackets.

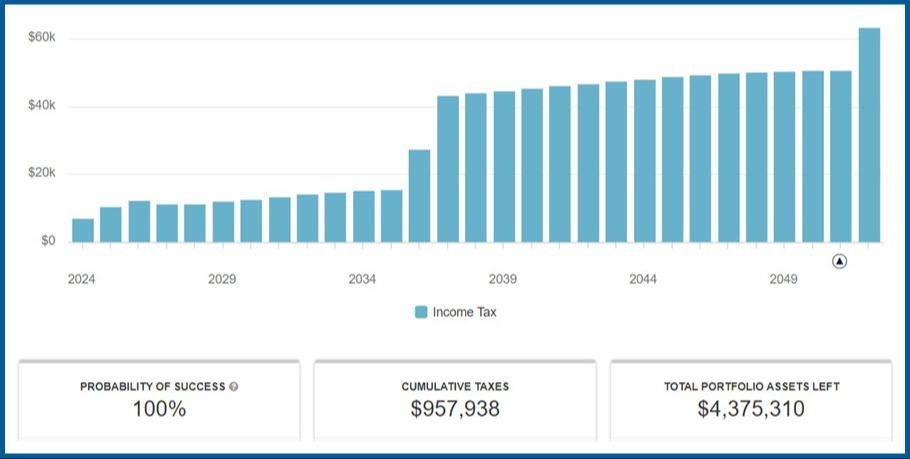

There may be strategies to pay a lower total amount of taxes over their lifetime. Roth conversions in the early retirement years may be an effective strategy to reduce taxes paid over a lifetime. Figure 1 below shows an example of the estimated yearly taxes expected to be paid over their lifetime. Note the increase midway based on the minimum distributions starting in 2036.

Figure 1. Software used by FJP to calculate the amount of taxes paid annually over a lifetime for a fictional client.

We have some clients who have a goal to leave money to their kids with as little tax liability as possible. Their adult kids may be professionals in high tax brackets and leaving IRA money to them could result in required distributions from the beneficiary IRAs that push them into even higher tax brackets.

Many people have a traditional pretax IRA and an after-tax Roth IRA. Strategies to reduce the tax liability on inherited money include spending the IRA money first. The money left to beneficiaries would then be in the Roth IRA which will pass tax-free to the heirs.

The non-retirement trust accounts get a step-up in cost basis at the date of death. A step-up in cost basis means the taxable gain that was in a trust account is stepped up to the value of the investment at the date of death. This results in no taxes due on that investment as of the date of death.

Understanding your current situation and intentions for passing money to your beneficiaries can significantly change the strategy you use with your assets to create income for you during retirement.

What if Tax Rates Go Up in the Future?

Another issue that could affect your plan for income during retirement is changes in tax rates over the next several decades. The U.S. Federal Government has been running very large deficits in recent years. We think the size of these large deficits is unsustainable. If that is true, then there is a good chance that tax rates could go up in the future.

If your goal is to reduce the total amount of taxes you pay over your lifetime, then it may make sense to use more of the taxable money now (such as money in an IRA) and pay the tax on the money as it comes out of the account now, at potentially lower tax rates. Then, you can leave non-taxed money in Roth accounts and possibly lower-taxed money in non-retirement accounts for use when you are older.

What About IRMAA?

IRMAA is the acronym for the income-related monthly adjustment amount. It is an extra premium that some Medicare Part B and D enrollees must pay in addition to their standard Medicare premium. The Social Security Administration (SSA) determines who pays IRMAA based on their income from two years prior. The income level where you start paying IRMAA changes each year. See your tax professional for the annual thresholds.

When money comes out of your IRA, it is taxed at the ordinary income rate. If you want to keep the IRMAA low, then you will need to keep the amount of money that you take out of your IRA low because this money is taxed as ordinary income, and your ordinary income determines how much you pay for IRMAA. The income level where you start paying IRMAA changes each year. In 2024, the thresholds to start paying IRMAA start at $103,000 for a single person and $206,000 for a married couple.

Should I Do a Roth Conversion?

A Roth Conversion takes money from your pre-tax IRA and moves it to your Roth IRA.

Anyone can do a Roth conversion, regardless of income or tax filing status. A rule for Roth Conversions is that if you withdraw the converted funds less than five years after they were converted, you will have a 10% penalty on the withdrawn earnings. When you do a Roth Conversion, the amount moved from the IRA to the Roth is considered taxable income. It is added to your total taxable income for that year. It can push you above the limit and cause you to pay the additional IRMAA if you are 65 and older and paying for Medicare.

We have seen this strategy work well for people in their early retirement years. If you are younger than 73, you are not required to take the required minimum distributions (RMDs) from your IRA. You may be retired, younger than 73, and in a low tax bracket. Your tax bracket may increase when you turn 73 and are forced to start taking money from your IRA. From the time you retire until you turn 73, we recommend evaluating doing a Roth Conversion each year to see if it makes sense.

How Do Market Corrections and Recessions Affect My Plan?

If this is not complicated enough, what happens if there is a significant market correction or recession during my retirement? The U.S. stock market experienced significant corrections of 25 to 50 percent during 2000-2002, 2008-2009, 2020 and 2022. If you are withdrawing money from accounts that are going down at the same time, this can have a very damaging impact on the value of your overall portfolio.

Some strategies can mitigate this, such as keeping enough money outside the stock market for your monthly income. Doing this can keep you from having to withdraw from your investments when they are down, thus giving them time to recover from the market correction. Our experience has shown that it is also helpful to reduce spending and the money you withdraw from accounts as much as possible in years when there is a significant stock market correction. We also recommend using an active management approach with your investments to sell and protect your investments somewhat during large market corrections.

How Do I Find the Best Retirement Income Plan for Me?

If you have some of the income sources and assets listed above, it can be difficult to determine your best strategy. We have found that the best way to complete the analysis to determine the strategies that best align with your goals is to create a comprehensive financial plan.

We use several software tools designed to consider client goals and the issues and strategies above to optimize each client's best retirement income plan. Since client goals and markets can change over time, we believe regularly working with clients to review and update their retirement income plans is important. We aim to help you achieve even more than you thought possible.

Helping you say, "I’m glad I did" instead of "I wish I had."

Our experience has shown that picking the right or wrong retirement income distribution strategies can change the value of a client's portfolio by hundreds of thousands of dollars over their lifetime. Different strategies can also significantly affect the total taxes paid over a lifetime. Developing your optimal retirement income plan is far too important to leave this to chance or guess what is best. Selecting the right or wrong strategies can make the difference between achieving or not achieving your goals in retirement.

We encourage you to work with a trained financial professional with the experience and tools to help you select the best retirement income plan for you. We regularly work with our clients on their retirement income plans to ensure they are updated as situations and goals change. If you are not a client and would like our help, give us a call at 408-963-2855 or schedule a complimentary introductory call.

We help our clients make smart decisions, such as creating an optimized retirement income plan that aligns their money with their goals so they can enjoy the journey.

Financial Journey Partners - Partners in Your Financial Journey®

Our Financial Journey Partners office is based in San Jose, California. We have clients that live in many states across the country. If you have questions about your investments or financial situation, call us to schedule time to talk about your specific situation.

Sign up for our email newsletter to stay up to date on our views of the economy, stock market, and top news stories.