Starting this January, you'll see some significant updates to the Federal tax code. Many of these changes come from last year's One Big Beautiful Bill (OBBB) Act, and there is quite a bit to unpack.

We recently came across a really helpful summary from Horsesmouth.com that does a great job breaking down the key highlights. They’ve given us permission to share it with you here.

One thing we need to mention: Tax law is incredibly complex. Between the official code, Treasury regulations, IRS rulings, and case law, the details can get tangled up quickly. This article gives you a solid overview, but if you have questions about how these changes affect your specific situation, we strongly recommend that you speak with a tax professional who can give you personalized guidance.

In this blog, we will discuss the following:

- Increase in the Standard Deduction

- Tax Brackets Changes

- Income Rates for Trusts

- 2026 Long-Term Capital Gains Rates and Qualified Dividends

- Retirement Plan Contribution Limits

- Additional Changes

- OBBB Temporary Changes

- Summary

Sign up for our email newsletter for views of the economy, stock market, and top news stories from our Wealth Managers at Financial Journey Partners.

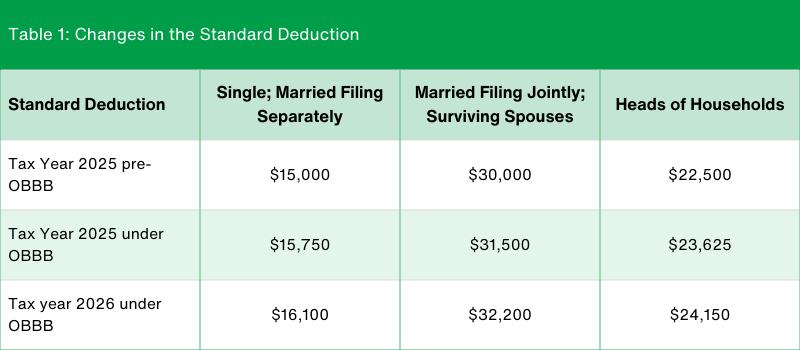

Increase the Standard Deduction

One notable change is the increase in the standard deduction for taxpayers who do not itemize. This adjustment is part of the annual inflation indexing. In addition, the standard deduction received an extra boost for tax year 2025 under the One Big Beautiful Bill (OBBB) Act.

Source: IRS

The OBBB ACT also raised the deduction cap for state and local taxes from 10,000 ($5,000 married filing separately) to $40,000 ($20,000 married filing separately) for taxpayers earning less than $500,000 in 2025, with the cap rising by 1% annually through 2029. The new cap phases out from $500,000 to $600,000 for all filers.

But this is a temporary feature. Beginning in 2030, the cap reverts to $10,000 ($5,000 married filing separately).

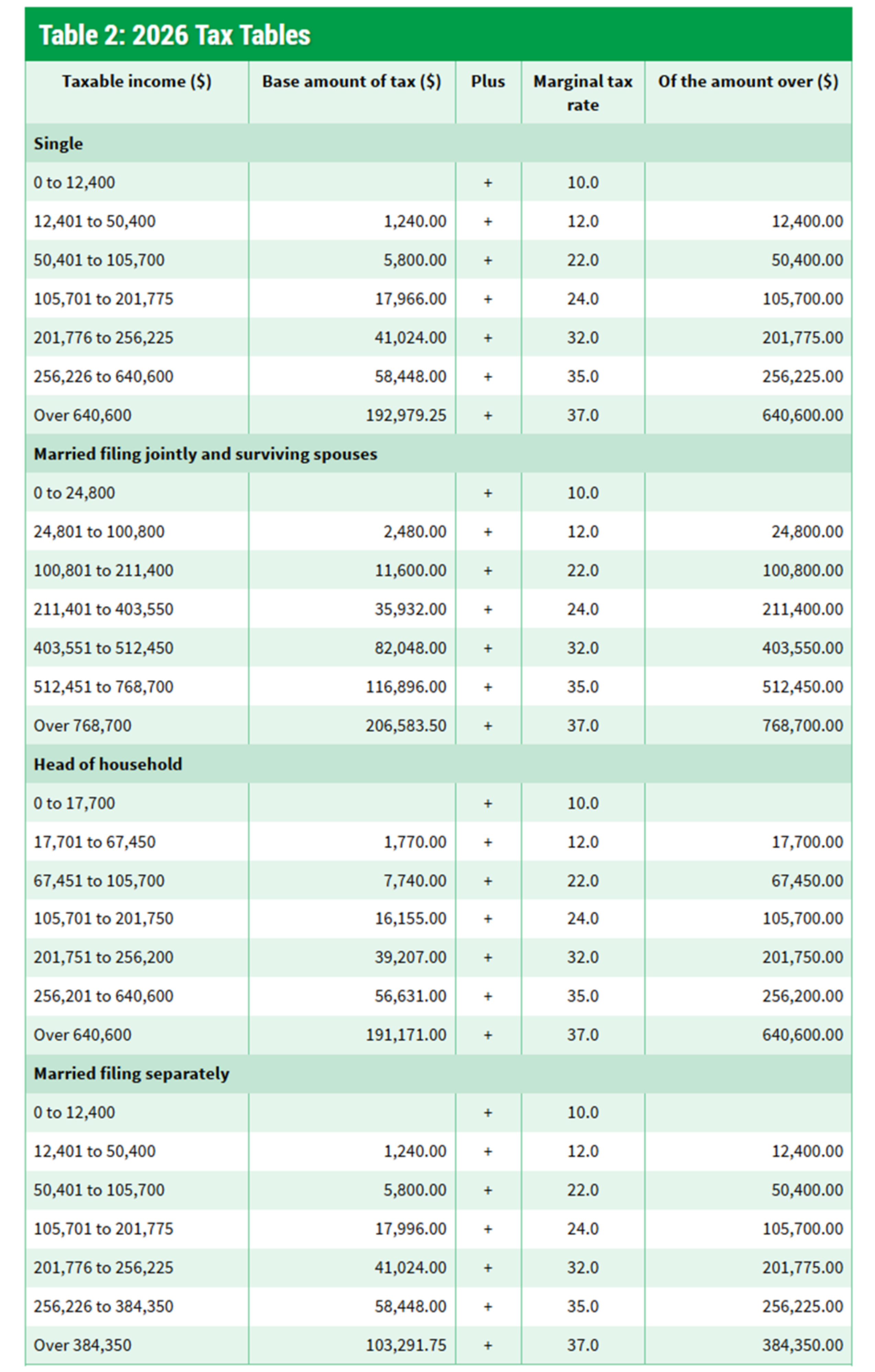

Tax Brackets Have Changed

Table 2 highlights the seven tax brackets for 2025 for single, married, head-of-household, and married filing separately. The OBBB Act permanently extended the brackets, which were set to expire in 2025 and return to pre-2018 levels. The seven brackets were established when the Tax Cuts and Jobs Act was passed in 2017.

Source: Tax Foundation, Fidelity

Generally speaking, the rates in Table 2 are applied to taxable income – income less the standard deduction or itemized deductions, whichever is higher. Taxable income is located on line 15 of Form 1040 2024 (2025 has not yet been published). It reads, “This is your taxable income.”

As an example, if you are married and filing jointly and your taxable income is $50,000, the first $24,800 is taxed at 10%, and the remaining is taxed at 12%. Tax credits and self-employment tax are not included. A tax credit reduces your tax liability dollar for dollar.

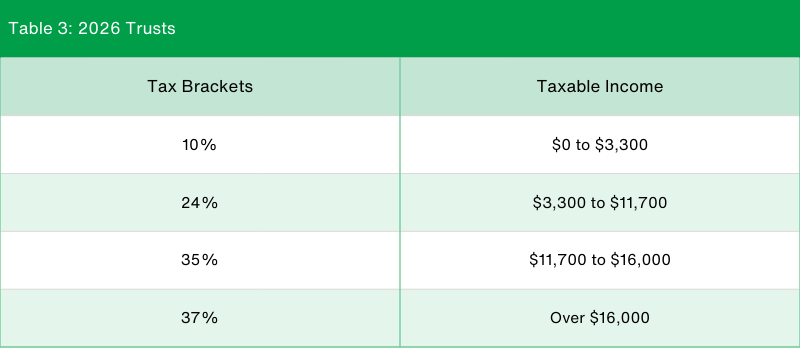

Income Tax Rates for Trusts

Table 3 illustrates the income rates for trusts.

Source: SmartAsset

The standard rules apply for these four tax brackets.

Retirement Plan Contribution Limits

Here are some of the key changes to the retirement plan contribution limits.

For 2026, the IRA contribution limits are $7,500 for those under age 50 and $8,600 for those age 50 or older. That is up $500 and $600, respectively, from 2025. The SEP IRA contribution limit for 2026 is 25% of eligible employee compensation, up to $72,000.

If you are self-employed, you may make an employer contribution on your own behalf. If you're self-employed, your contributions are generally limited to 20%, or up to $72,000 of compensation.

There are also changes to the 401(k) and 403(b) contributions limits, plus changes to the catch-up amounts. See this table for the details.

2026 Long-Term Capital Gains Rates and Qualified Dividends

Favorable treatment for long-term capital gains and qualified dividends is available. Long-term capital gains, such as the profit on the sale of a stock held for more than one year, are taxed at a more favorable rate than short-term gains. A short-term gain is taxed as ordinary income.

Source: Fidelity, IRS

Additional Changes

Below are additional changes to the tax laws for 2026.

- For tax year 2026, the alternative minimum tax exemption amount for unmarried individuals is $90,100 and begins to phase out at $500,000 ($142,200 for married couples filing jointly, for whom the exemption begins to phase out at $1,000,000).

- The child tax credit is $2,200 per qualifying child. If you have little or no federal income tax liability, you may qualify for the Additional Child Tax Credit (ACTC), up to $1,700 per qualifying child depending on your income. You must have earned income of at least $2,500 to be eligible for the ACTC. Your qualify for the full child tax credit for each qualifying child if you meet all eligibility factors and your annual income is not more than $200,000 ($400,000 if filing a joint return).

- The estate exemption for individuals in 2025 is $15 million, up from a total of $13,999,000 for estates of decedents who died in 2025.

- The annual gift tax exclusion for 2026 remains $19,000 without using any of the lifetime gift and estate tax exemption. If a gift tops $19,000, the excess amount can be subtracted from your lifetime gift and estate tax exemption.

- If your health insurance plan allows for a Health Savings Account, the contribution limit for 2026 is $4,400 for self-only coverage and $8750 for family coverage. The limits are up $100 and $200, respectively, from 2025. Those 55 and older who are not enrolled in Medicare can contribute an additional $1,000 as a catch-up contribution. A married couple can combine their exclusions to gift up to $38,000 per recipient per year. There is no limit for tuition and medical expenses.

Other taxes you may be subject to or credits you may capture.

- High-income taxpayers are subject to the net investment income tax of 3.8%, levied on the lesser of net investment income or the excess of modified adjusted gross income (MAGI) over the following threshold amounts: $200,000 for single and head of household filers, $250,000 for married filing jointly or qualifying surviving spouse, and $125,000 for married filing separately.

- These amounts have never been indexed to inflation. In general, net investment income includes but is not limited to interest, dividends, capital gains, rental, and royalty income, and non-qualified annuities, according to the IRS. Net investment income generally does not include wages, unemployment compensation, Social Security benefits, alimony, and most self-employment income.

- A new wrinkle created by the OBBB Act will benefit most taxpayers. Beginning in 2026, those who claim the standard deduction may deduct up to $1,000 in qualified charitable donations ($2,000 if filing jointly). The deduction applies only to cash donations.

- Do you itemize? Beginning in tax year 2026, you may only deduct charitable gifts that surpass 0.5% of your adjusted gross income. In addition, the new law caps the value of all itemized charitable deductions at 35% for taxpayers in the highest income bracket (37%).

- For tax year 2026, the maximum credit allowed for adoptions for a special needs child is the amount of qualified adoption expenses up to $17,670, up from $17, 280 in 2025. For tax year 2026, the amount of credit that may be refundable is $5,120.

Income phase-out: The credit starts to phase out if your modified adjusted gross income is above $265,080 and is fully phased out at $305,080.

OBBB Temporary Changes

Beyond the temporary change to the deduction for state and local taxes, the OBBB Act includes temporary changes to the tax code that run through 2028.

These include the following.

- No Tax on Tips: Employees and self-employed individuals may deduct qualified tips received in occupations that are listed by the IRS as customarily and regularly receiving tips on or before December 31, 2024. Phaseouts begin when adjusted gross income exceeds $150,000 ($300,000 for join filers).

- No Tax on Overtime: Qualified overtime wages that exceed the regular pay rate avoid federal income tax. For example, if you earn $20 per hour and are paid a total of $30 per hour when working overtime, only the extra $10 per hour counts toward the deduction. If you earn double time at $40 per hour, the deductible portion is still $10 per hour. Taxes will be withheld on the entire amount, and workers may deduct qualified overtime, which will be reflected on their W-2. Employees must work more than 40 hours a week to qualify. For example, if an employee earns time-and-a-half for six hours but only works 35 hours that week, they are not eligible for the tax deduction. The exemption is capped at $12,500 per individual (or $25,000 per couple). The deduction phases out for taxpayers with modified adjusted gross income over $150,000 ($300,000 for joint filers).

- Newborn Savings: Provided both parents are U.S. citizens and have a Social Security number, children born between 2025 and 2028 will be automatically enrolled in a federal savings account, dubbed “Trump Accounts,” with a one-time $1,000 deposit. These accounts allow for annual contributions of up to $5,000 (indexed for inflation). The account grows tax-deferred until withdrawals begin—allowed starting at age 18—at which point, it essentially follows the rules for an IRA.

- Enhanced Deduction for Seniors: Seniors aged 65 and older will receive an additional $6,000 deduction. There is a $12,000 deduction for married taxpayers if both spouses are 65 or older and filing jointly. This benefit applies to standard and itemized filers but begins to phase out for individuals with modified adjusted gross income of more than $75,000 and $150,000 for joint filers.

- No Tax on Car Loan Interest: Effective for 2025 through 2028, individuals may deduct interest paid on a loan used to purchase a qualified vehicle, provided the car is purchased for personal use and meets other eligibility criteria (lease payments do not qualify). The vehicle must have “undergone final assembly in the U.S.,” per the IRS. The maximum annual deduction is $10,000.

Summary

Feeling a bit overwhelmed? You’re not alone. These are substantial changes-even the tax professionals we talk with are finding them challenging to navigate. Many are attending multiple training sessions this year just to stay on top of everything and to be ready for tax season.

Our advice: If you work with a tax professional, reach out early this year. With so many new rules in play, they’re likely to be busier than usual, and you’ll benefit from getting on their calendar sooner rather than later.

And if you’ve been handling your own taxes up until now, this might be the year to bring in some expert support-it could save you time, stress, and potentially money too.

As always, if there is anything we can do to help you, give your Wealth Manager a call. If you would like to be introduced to a tax professional, we have vetted people that may be able to help you and we are happy to introduce you to them.

Over the next several months, we will keep you informed when your tax documents are ready from Fidelity in January and February. They estimate the1099R for retirement accounts will be available before Jan 31. Non-retirement accounts will likely come out between Feb 12 and Feb 22. Some could be later based on unusual holdings. Once Fidelity has created your tax documents, they will mail them to you if you selected to have them delivered to you by mail. Remember your tax documents can be accessed by everyone in the vault, in your client portal, as soon as they are available.

Schedule Your Complementary Initial Consultation (https://www.financialjourney.com/schedule-consultation)

For our clients, if you want to talk more about your specific situation, contact your Wealth Managers Elaine Manley, Scott Manley or Linda Tjiputra.

Investment advisory services offered through Mutual Advisors, LLC DBA Financial Journey Partners, an SEC Registered Investment Adviser. Securities offered through Mutual Securities, Inc., Member FINRA/SIPC. Mutual Securities, Inc. and Mutual Advisors, LLC are affiliated companies.